ご利用について

This PDQ cancer information summary for health professionals provides comprehensive, peer-reviewed, evidence-based information about the treatment of colon cancer. It is intended as a resource to inform and assist clinicians who care for cancer patients. It does not provide formal guidelines or recommendations for making health care decisions.

This summary is reviewed regularly and updated as necessary by the PDQ Adult Treatment Editorial Board, which is editorially independent of the National Cancer Institute (NCI). The summary reflects an independent review of the literature and does not represent a policy statement of NCI or the National Institutes of Health (NIH).

CONTENTS

- Financial Toxicity Associated With Cancer Care—Background and Prevalence

-

Introduction

A number of studies demonstrate that individuals with cancer are at higher risk of experiencing financial difficulty than are individuals without cancer.[ 1 ][ 2 ][ 3 ][ 4 ][ 5 ][ 6 ][ 7 ] This summary reviews the extant literature on financial toxicity among American cancer patients and survivors.

Background

Cancer is one of the most costly medical conditions to treat in the United States.[ 8 ] Cancer patients can receive multiple types of treatment, including surgery, radiation therapy, and systemic treatment. Historically, inpatient hospitalizations have been the major drivers of the costs of cancer care. Compared to a decade ago, cancer patients are receiving increasingly expensive chemotherapy and biologics, both alone and in combination.[ 9 ][ 10 ] The use of expensive supportive agents and hematopoietic growth factors has also increased.[ 9 ] The list price of newly introduced systemic therapies and supportive drug-based treatments is growing,[ 9 ][ 10 ][ 11 ] and prices of both infusion and oral drugs continue to increase after product launch.[ 12 ][ 13 ] Although prices can vary dramatically among treatments, often data are lacking about the differences in outcomes. Prices higher than $10,000 a month for individual drugs and biologic agents are common.

At the same time, commercial insurers in the United States are shifting more direct medical care costs to patients through higher premiums, deductibles, and coinsurance and copayment rates. The 2016 Commonwealth Fund Biennial Health Insurance Survey indicated that 33% of insured adults aged 19 to 64 years had medical bill problems or accrued medical debt.[ 14 ] Infused chemotherapy and supportive agents covered under patients’ medical benefits entail high out-of-pocket costs; these costs also appear to be growing as care shifts from the community into hospital-based outpatient departments.

Oral cancer drug–based treatments are frequently covered under patient pharmacy benefits’ specialty tier, requiring high coinsurance that patients pay out of pocket. High cost-sharing plans, including tiered outpatient prescription formularies (i.e., copays that escalate depending on whether the drug is generic or branded, and by price) may be particularly troublesome for patients with cancer who are prescribed expensive oral chemotherapeutics. The proportion of health care plans with multitiered (>3) prescription formularies, in which expensive oral specialty drugs are associated with the highest cost sharing, increased from 3% in 2004 to nearly 88% in 2017.[ 15 ] These trends in treatment cost and changes in insurance coverage suggest that financial distress associated with acute and chronic cancer is highly prevalent, even among persons with health insurance.

When compared with individuals without a cancer history, cancer survivors have higher out-of-pocket costs, even many years after initial diagnosis,[ 1 ][ 2 ][ 3 ][ 4 ] reflecting ongoing cancer care and care for any late or lasting treatment effects. In addition, cancer survivors are more likely to report being unable to work because of their health,[ 1 ][ 2 ][ 3 ][ 4 ] including more missed work days or additional days spent in bed because of poor health.[ 1 ][ 2 ][ 3 ][ 4 ] Limited ability to work may also reduce employment-based health insurance options and resources to pay for medical care, further magnifying the financial impact of cancer. Combined, these factors contribute to the phenomenon of adverse financial effects of cancer treatment.

A number of terms have been used to describe the financial impact of cancer, its treatment, and the lasting effects of treatment, including financial distress, financial stress, financial hardship, financial toxicity, financial burden, economic burden, and economic hardship.[ 16 ][ 17 ]

Etiology and Risk Factors

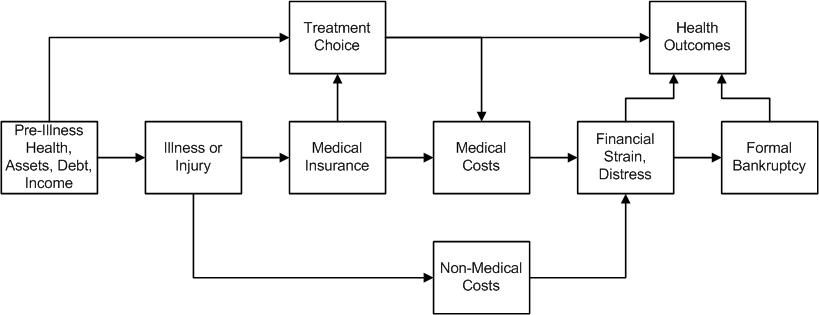

The interplay between cancer and financial distress is complex and related to a number of factors, as shown in Figure 1.[ 18 ][ 19 ]

Figure 1. Conceptual framework relating severe illness, treatment choice, and health and financial outcomes. Credit: Scott Ramsey, MD, PhD. Several factors in a household at the time a member of that household is diagnosed with cancer will influence the vulnerability to financial distress. The risk of severe distress and the period between illness and these outcomes will be influenced by the following factors:

At the time of cancer diagnosis, several factors that determine the long-range risk of financial hardship include the following:

Components of these measures include material conditions that arise from increased out-of-pocket expenses, lower income from the inability to work, and psychological response to increased household expenses and reduced income.[ 16 ][ 17 ]

The material conditions of patients and their families that may be adversely affected by a cancer diagnosis and treatment are typically measured as follows:[ 16 ][ 17 ]

In addition, a patient's psychological response to increased financial burden associated with a cancer diagnosis and treatment is typically measured as financial stress, distress, or worry.[ 16 ][ 17 ]

Prevalence

A number of studies have measured components of at least one aspect of financial hardship,[ 1 ][ 4 ][ 5 ][ 6 ][ 20 ][ 21 ][ 22 ][ 23 ][ 24 ][ 25 ][ 26 ][ 27 ][ 28 ][ 29 ][ 30 ][ 31 ][ 32 ] although methods and measures vary widely, limiting comparisons across studies. In addition, most studies that have evaluated financial hardship were conducted at single institutions, which are geographically defined, or in other selected samples of cancer survivors. Nationally representative estimates of financial hardship from survey data are generally reported for all cancer survivors, and scant information is available by cancer site or stage of disease at diagnosis. Household surveys generally include few newly diagnosed cancer patients, those with rare cancers, or those with projected short-term survival. Because data about financial hardship are not routinely collected and can be difficult to measure, few studies have reported incidence of financial hardship among the newly diagnosed or newly treated.

The following sections describe the prevalence of specific measures of financial hardship, including out-of-pocket costs, productivity loss, asset depletion and medical debt, bankruptcy, and financial distress and worry.

Prevalence of high out-of-pocket costs

Out-of-pocket costs are one of the most common measures of financial hardship and are the amounts that patients pay directly for their medical care, including insurance copayments, coinsurance, and deductibles for prescription and nonprescription medications, hospitalizations, outpatient services, and other types of medical care.[ 17 ] Cancer survivors generally report higher out-of-pocket expenditures than do individuals without a cancer history.[ 1 ][ 2 ][ 3 ][ 7 ][ 20 ] In a nationally representative sample, recently diagnosed cancer survivors aged 18 to 64 years reported $1,107 annual in out-of-pocket spending, compared with $747 annually for previously diagnosed cancer survivors and $617 annually for those without a cancer history (all in 2010 dollars).[ 2 ]

In a study of long-term breast cancer survivors, 18% paid $2,100 to less than $5,000 in out-of-pocket expenses, and 17% paid more than $5,000.[ 24 ] Cancer survivors are also more likely to report a high out-of-pocket burden (i.e., annual out-of-pocket health care spending >20% of annual income) than individuals without a cancer history,[ 4 ][ 5 ][ 6 ] although estimates vary widely, reflecting differences in population characteristics.

In a study conducted using the nationally representative Medical Expenditure Panel Survey (MEPS), 4.3% of cancer survivors aged 18 to 64 years reported high out-of-pocket burden compared with 3.4% of those without a cancer history.[ 4 ] In a study using the nationally representative Medicare Current Beneficiary Survey, 28% of cancer survivors reported high out-of-pocket burden compared with 16% of those without a cancer history.[ 6 ] Approximately 84% of the Medicare beneficiaries were aged 65 years and older.

Prevalence of productivity loss

Productivity loss is typically measured as the inability to work or pursue usual activities, days lost from work or disability days, reduction in work hours, and days spent in bed. Productivity loss may be quantified directly from employment data [ 22 ][ 31 ] or estimated with median wages.[ 1 ][ 2 ][ 3 ] Several studies have used data from the nationally representative MEPS. Using data from the Panel Study of Income Dynamics, a nationally representative, prospective, population-based observational study, one study found that the probability of being employed among persons reporting a cancer diagnosis decreased 9 percentage points 3 years from the date of diagnosis, with no recovery for those alive in years 4 and 5. During this time, survivors’ labor market earnings dropped by up to 40%. Family income dropped by 20% during this time but recovered by year 4.[ 33 ] Another analysis reported that, among the employed, those receiving cancer care missed 22.3 more workdays per year than individuals without any cancer treatment.[ 34 ] An estimated productivity loss for adult survivors of adolescent and young adult cancers was $4,564 compared with $2,314 for adults without a cancer history (in 2011 dollars).[ 3 ] Employed cancer survivors reported cancer interfered with physical tasks (25%) and mental tasks (14%) required by their jobs.[ 1 ]

Prevalence of asset depletion and medical debt

Several studies have reported the prevalence of asset depletion and medical debt for cancer survivors, although this information is rarely reported in relation to individuals without a cancer history or before and after a cancer diagnosis. Further, most estimates are based on self-report, and little validation work has been conducted.

Studies of cancer survivors have suggested that between 33% and 80% of the survivors have used savings to finance medical expenses,[ 20 ][ 24 ][ 28 ][ 30 ][ 32 ] and between 2% and 34% have borrowed money to pay for their care or have medical debt.[ 21 ][ 24 ][ 25 ][ 26 ][ 28 ] In a study of women with breast cancer, self-reported debt varied by race and ethnicity, with 27.1% of white, 58.9% of black, 33.5% of Latina, and 28.8% of Asian women reporting treatment-related debt.[ 35 ] In a study of colon cancer survivors in Washington state, the mean debt among the survivors with debt was $26,860 (in 2009 dollars).[ 28 ] To cope with expenses, cancer survivors have reported decreasing spending on leisure activities, food, clothing, and utilities; selling stocks, investments, possessions, or property; and changing housing.[ 24 ][ 28 ][ 30 ][ 32 ][ 34 ][ 35 ]

Incidence and prevalence of bankruptcy

One of the few studies to measure the incidence of financial hardship reported that 1.7% of cancer survivors filed for bankruptcy in the 5 years after diagnosis.[ 27 ] Cancer survivors were 2.7 times more likely to file for bankruptcy than individuals without a cancer history.[ 27 ] Others have reported a prevalence of bankruptcy ranging from 1.2% to 3% of the study populations of cancer survivors.[ 20 ][ 21 ][ 26 ][ 36 ]

Prevalence of financial stress, distress, or worry

Several studies have found a prevalence of financial stress and worry about paying medical bills for cancer ranging from 22.5% in a nationally representative sample [ 21 ] to 64% in a sample of working-age cancer survivors.[ 21 ][ 23 ] About 45% of cancer survivors recruited from a single outpatient oncology clinic study reported wage concerns.[ 23 ] In one study, respondents reported being at least somewhat worried about finances as a result of breast cancer or its treatment, with 31.9% of white, 48.9% of black, 49.7% of Latina, and 35.2% of Asian women reporting at least some worry.[ 35 ] Patients and their families may also experience difficulty and stress in interpreting complex medical bills, although this stress is less studied.

Prevalence of financial hardship as a composite measure

Several studies combine multiple components of financial hardship using summary measures, scores, or measures, including the Comprehensive Score for Financial Toxicity (COST) measure and the Personal Financial Wellness (PFW) Scale (formerly known as the InCharge Financial Distress/Financial Well-Being (IFDFW) Scale, but the results are rarely presented in relation to the general population and can be difficult to interpret.

In a study of multiple myeloma patients undergoing treatment at a single academic cancer center, cancer survivors had a mean COST score of 23 (score range, 0–44, with lower values equivalent to higher burden).[ 37 ] Another study used the IFDFW Scale in a convenience sample of cancer patients receiving radiation therapy or chemotherapy at a single outpatient cancer center and found an average financial distress score of 5 [ 17 ] (score range, 1–10, with lower numbers indicating higher distress).[ 25 ] In other studies, financial burden scores were based on the count of affirmative responses to a series of questions,[ 26 ][ 30 ][ 34 ] and the mean number (e.g., 2.94 economic burden items related to work and hardship events) was calculated.[ 26 ]

参考文献- Ekwueme DU, Yabroff KR, Guy GP, et al.: Medical costs and productivity losses of cancer survivors--United States, 2008-2011. MMWR Morb Mortal Wkly Rep 63 (23): 505-10, 2014.[PUBMED Abstract]

- Guy GP, Ekwueme DU, Yabroff KR, et al.: Economic burden of cancer survivorship among adults in the United States. J Clin Oncol 31 (30): 3749-57, 2013.[PUBMED Abstract]

- Guy GP, Yabroff KR, Ekwueme DU, et al.: Estimating the health and economic burden of cancer among those diagnosed as adolescents and young adults. Health Aff (Millwood) 33 (6): 1024-31, 2014.[PUBMED Abstract]

- Guy GP, Yabroff KR, Ekwueme DU, et al.: Healthcare Expenditure Burden Among Non-elderly Cancer Survivors, 2008-2012. Am J Prev Med 49 (6 Suppl 5): S489-97, 2015.[PUBMED Abstract]

- Bernard DS, Farr SL, Fang Z: National estimates of out-of-pocket health care expenditure burdens among nonelderly adults with cancer: 2001 to 2008. J Clin Oncol 29 (20): 2821-6, 2011.[PUBMED Abstract]

- Davidoff AJ, Erten M, Shaffer T, et al.: Out-of-pocket health care expenditure burden for Medicare beneficiaries with cancer. Cancer 119 (6): 1257-65, 2013.[PUBMED Abstract]

- Langa KM, Fendrick AM, Chernew ME, et al.: Out-of-pocket health-care expenditures among older Americans with cancer. Value Health 7 (2): 186-94, 2004 Mar-Apr.[PUBMED Abstract]

- Soni A: Trends in the Five Most Costly Conditions among the U.S. Civilian Institutionalized Population, 2002 and 2012. Statistical Brief 470. Rockville, Md: Agency for Healthcare Research and Quality, 2015. Available online. Last accessed December 8, 2016.[PUBMED Abstract]

- Bradley CJ, Yabroff KR, Warren JL, et al.: Trends in the Treatment of Metastatic Colon and Rectal Cancer in Elderly Patients. Med Care 54 (5): 490-7, 2016.[PUBMED Abstract]

- Shih YC, Smieliauskas F, Geynisman DM, et al.: Trends in the Cost and Use of Targeted Cancer Therapies for the Privately Insured Nonelderly: 2001 to 2011. J Clin Oncol 33 (19): 2190-6, 2015.[PUBMED Abstract]

- Conti RM, Fein AJ, Bhatta SS: National trends in spending on and use of oral oncologics, first quarter 2006 through third quarter 2011. Health Aff (Millwood) 33 (10): 1721-7, 2014.[PUBMED Abstract]

- Gordon N, Stemmer SM, Greenberg D, et al.: Trajectories of Injectable Cancer Drug Costs After Launch in the United States. J Clin Oncol 36 (4): 319-325, 2018.[PUBMED Abstract]

- Shih YT, Xu Y, Liu L, et al.: Rising Prices of Targeted Oral Anticancer Medications and Associated Financial Burden on Medicare Beneficiaries. J Clin Oncol 35 (22): 2482-2489, 2017.[PUBMED Abstract]

- 2016 Biennial Health Insurance Survey. New York, NY: The Commonwealth Fund, 2017. Available online. Last accessed December 13, 2018.[PUBMED Abstract]

- 2017 Employer Health Benefits Survey. San Francisco, Calif: Henry J. Kaiser Family Foundation, 2017. Available online. Last accessed December 13, 2018.[PUBMED Abstract]

- Tucker-Seeley RD, Yabroff KR: Minimizing the "financial toxicity" associated with cancer care: advancing the research agenda. J Natl Cancer Inst 108 (5): , 2016.[PUBMED Abstract]

- de Souza JA, Yap B, Ratain MJ, et al.: User beware: we need more science and less art when measuring financial toxicity in oncology. J Clin Oncol 33 (12): 1414-5, 2015.[PUBMED Abstract]

- Smith R, Clarke L, Berry K, et al.: A comparison of methods for linking health insurance claims with clinical records from a large cancer registry. [Abstract] Med Decis Making 21 (6): 530, 2001.[PUBMED Abstract]

- Fay S, Hurst E, White MJ: The household bankruptcy decision. Am Econ Rev 92 (3): 706-18, 2002.[PUBMED Abstract]

- Banegas MP, Guy GP, de Moor JS, et al.: For Working-Age Cancer Survivors, Medical Debt And Bankruptcy Create Financial Hardships. Health Aff (Millwood) 35 (1): 54-61, 2016.[PUBMED Abstract]

- Yabroff KR, Dowling EC, Guy GP, et al.: Financial Hardship Associated With Cancer in the United States: Findings From a Population-Based Sample of Adult Cancer Survivors. J Clin Oncol 34 (3): 259-67, 2016.[PUBMED Abstract]

- Chang S, Long SR, Kutikova L, et al.: Estimating the cost of cancer: results on the basis of claims data analyses for cancer patients diagnosed with seven types of cancer during 1999 to 2000. J Clin Oncol 22 (17): 3524-30, 2004.[PUBMED Abstract]

- Ell K, Xie B, Wells A, et al.: Economic stress among low-income women with cancer: effects on quality of life. Cancer 112 (3): 616-25, 2008.[PUBMED Abstract]

- Jagsi R, Pottow JA, Griffith KA, et al.: Long-term financial burden of breast cancer: experiences of a diverse cohort of survivors identified through population-based registries. J Clin Oncol 32 (12): 1269-76, 2014.[PUBMED Abstract]

- Meisenberg BR, Varner A, Ellis E, et al.: Patient Attitudes Regarding the Cost of Illness in Cancer Care. Oncologist 20 (10): 1199-204, 2015.[PUBMED Abstract]

- Meneses K, Azuero A, Hassey L, et al.: Does economic burden influence quality of life in breast cancer survivors? Gynecol Oncol 124 (3): 437-43, 2012.[PUBMED Abstract]

- Ramsey S, Blough D, Kirchhoff A, et al.: Washington State cancer patients found to be at greater risk for bankruptcy than people without a cancer diagnosis. Health Aff (Millwood) 32 (6): 1143-52, 2013.[PUBMED Abstract]

- Shankaran V, Jolly S, Blough D, et al.: Risk factors for financial hardship in patients receiving adjuvant chemotherapy for colon cancer: a population-based exploratory analysis. J Clin Oncol 30 (14): 1608-14, 2012.[PUBMED Abstract]

- Regenbogen SE, Veenstra CM, Hawley ST, et al.: The personal financial burden of complications after colorectal cancer surgery. Cancer 120 (19): 3074-81, 2014.[PUBMED Abstract]

- Veenstra CM, Regenbogen SE, Hawley ST, et al.: A composite measure of personal financial burden among patients with stage III colorectal cancer. Med Care 52 (11): 957-62, 2014.[PUBMED Abstract]

- Wan Y, Gao X, Mehta S, et al.: Indirect costs associated with metastatic breast cancer. J Med Econ 16 (10): 1169-78, 2013.[PUBMED Abstract]

- Zafar SY, Peppercorn JM, Schrag D, et al.: The financial toxicity of cancer treatment: a pilot study assessing out-of-pocket expenses and the insured cancer patient's experience. Oncologist 18 (4): 381-90, 2013.[PUBMED Abstract]

- Zajacova A, Dowd JB, Schoeni RF, et al.: Employment and income losses among cancer survivors: Estimates from a national longitudinal survey of American families. Cancer 121 (24): 4425-32, 2015.[PUBMED Abstract]

- Finkelstein EA, Tangka FK, Trogdon JG, et al.: The personal financial burden of cancer for the working-aged population. Am J Manag Care 15 (11): 801-6, 2009.[PUBMED Abstract]

- Jagsi R, Ward KC, Abrahamse PH, et al.: Unmet need for clinician engagement regarding financial toxicity after diagnosis of breast cancer. Cancer 124 (18): 3668-3676, 2018.[PUBMED Abstract]

- Meisenberg BR: The financial burden of cancer patients: time to stop averting our eyes. Support Care Cancer 23 (5): 1201-3, 2015.[PUBMED Abstract]

- Huntington SF, Weiss BM, Vogl DT, et al.: Financial toxicity in insured patients with multiple myeloma: a cross-sectional pilot study. Lancet Haematol 2 (10): e408-16, 2015.[PUBMED Abstract]

- Risk Factors Associated With Financial Toxicity

-

Several disease-related, sociodemographic, and health insurance–related factors have been implicated as contributors to increased risk of financial toxicity among cancer patients and survivors.

Disease- and Treatment-Related Risk Factors

Patients with advanced-stage cancers, cancers requiring chemotherapy or radiation therapy, and those with underlying comorbidities have been shown to have a higher risk of financial hardship after diagnosis than do those without these characteristics.[ 1 ][ 2 ][ 3 ][ 4 ] In a study of 1,556 cancer survivors identified from the 2010 National Health Interview Survey (NHIS) who responded to a single survey item assessing financial burden, survivors were more likely to report high financial burden if they received chemotherapy (47.2% vs. 30.8%; P < .001), received radiation therapy (44.7% vs. 31.4%; P < .001), and had recurrent or multiple cancers (40.9% vs. 33.7%; P < .049).[ 3 ]

A similar association was seen in an analysis using data from the 2008–2010 Medical Expenditures Panel Survey (MEPS) Household Component to measure loss of employment and productivity in individuals with and without cancer.[ 1 ] In this study, survivors with more-aggressive disease processes (i.e., recurrent cancer, multiple cancers, poor-prognosis cancers) had the highest rates of lost productivity relative to individuals without cancer. Specifically, individuals with cancers associated with short survival were less likely to be employed (66.8% vs. 81.4%; P < .0001) and more likely to face limitations on their ability to participate in activities at home, work, or school (17.5% vs. 8.5%; P < .001) compared with individuals without cancer. Productivity among survivors of breast, prostate, colorectal, and other single-cancers was not as decreased as productivity among those with higher-risk disease.

Another study used multiple years of the MEPS (2008‒2013) to evaluate the associations between cancer history, chronic conditions, and productivity losses.[ 5 ] Adult cancer survivors were significantly more likely to have chronic conditions, including heart disease, diabetes, asthma, and arthritis, than were adults without a cancer history. They were also more likely to have multiple chronic conditions. Cancer survivors who had multiple chronic conditions were more likely to be limited in their ability to work compared with cancer survivors without these other conditions. Among cancer survivors, those with four or more chronic conditions had annual productivity loss of $9,099 (95% confidence interval [CI], $7,224‒$10,973) compared with those without any additional chronic conditions (in 2013 dollars).

Receipt of cancer-directed treatment and the presence of other comorbidities were also found to be associated with higher out-of-pocket spending in the Medicare population. In a study using data from the Medicare Current Beneficiary Survey linked to Medicare claims (1997–2007), 2-year mean out-of-pocket spending was higher by $1,526 among patients receiving chemotherapy and $1,470 among patients receiving radiation therapy compared with patients who did not receive treatment (P < .01).[ 6 ]

These studies together suggest that cancer survivors across a broad age range with advanced cancers, recurrent cancers, or cancers that require treatment (likely a marker of more-advanced disease) are more likely to face higher out-of-pocket spending and are at higher risk of financial hardship. Chronic treatment-related spending in combination with inability to regain employment and income resulting from progressive disease and debility may contribute to the association between advanced disease and greater financial burden.

Sociodemographic Risk Factors

Age

A number of studies have consistently demonstrated an association between younger age at cancer diagnosis and higher risk of various types of financial hardship.[ 3 ][ 7 ][ 8 ][ 9 ][ 10 ][ 11 ] In the setting of a health shock such as cancer, younger individuals may be particularly vulnerable to financial hardships because of a lack of savings and assets, as well as competing financial obligations (e.g., children). Moreover, younger survivors lack the protection of Medicare coverage, placing some without insurance or with high-deductible health plans at risk of financial toxicity.

In a study of bankruptcy rates among western Washington residents with and without cancer, bankruptcy rates were highest among both cancer survivors and noncancer controls aged 20 to 34 years (10.06 and 3.15 per 1,000 person-years, respectively) and lowest among survivors and controls aged 80 to 90 years (0.94 and 0.57 per 1,000 person-years, respectively).[ 7 ] More notably, the relative risk of bankruptcy filing for cancer survivors versus controls increased with each younger-age cohort. Other studies have similarly shown that younger individuals with cancer are at higher risk of financial hardship.[ 3 ][ 9 ]

In an analysis of data from the 1,202 adult cancer survivors identified from the 2011 MEPS Experiences with Cancer questionnaire, material financial hardship (defined as bankruptcy, loans, debt, inability to pay for care, or making other financial sacrifices) was more common among cancer survivors younger than 65 years compared with those 65 years and older (28.4% vs. 13.8%; P < .001).[ 10 ] In a study of 4,719 adult cancer survivors aged 18 to 64 years who completed the 2012 Livestrong survey, debt and bankruptcy were higher among survivors aged 45 to 54 years (risk ratio, 1.66; P < .001) and aged 18 to 44 years (odds ratio [OR], 2.07; P < .001) compared with survivors aged 55 to 64 years.[ 8 ]

Accumulating evidence suggests that adult survivors of childhood cancers may be especially vulnerable to financial hardship.[ 11 ][ 12 ] A cancer diagnosis during childhood can interfere with physical, emotional, and mental development and disrupt education and limit employment opportunities. Childhood cancer survivors also face elevated risk of second cancers and other late and lasting effects of their treatment(s). Research from the Childhood Cancer Survivor Study found that adult survivors of childhood cancers were more likely to spend at least 10% of their annual incomes on out-of-pocket medical costs than their siblings (10.2% vs. 2.9%; P <.001).[ 12 ]

Financial hardship among younger patients, however, may not solely result from higher out-of-pocket spending for cancer care. In a study using data from the 2001–2008 MEPS, a higher proportion of individuals aged 55 to 64 years reported spending 20% or more of their incomes on health care and premiums relative to younger individuals aged 18 to 39 years (10.1% vs. 7.1%; P = .05). This discrepancy suggests that high out-of-pocket spending alone does not lead to financial hardship.

Income

As might be expected, cancer patients in lower-income household groups are also at increased risk of treatment-related financial hardship. No clear income threshold below which financial hardship risk markedly increases has been identified because annual household income has been categorized differently across studies. For example, in one study of nonelderly cancer patients (ages 18–64 years) identified from the 2012 Livestrong survey, income between $41,000 and $80,000 and income of $40,000 or below were both associated with increased risk of borrowing money or going into debt compared with income of $81,000 and higher (OR, 2.46 and 3.52, respectively; P < .0001).

Other studies have shown increased risk of financial hardship among individuals with household incomes below thresholds of $50,000 or $20,000.[ 9 ][ 13 ] However, there is currently no consensus about an absolute income below which patients face higher financial-hardship risk. In the Medicare population, this association also seems to hold true, with higher income (represented as percentages above the federal poverty level) being protective against high out-of-pocket cost burden.[ 6 ]

Race

Minority race has been shown to be strongly associated with disparities in cancer health outcomes, including survival.[ 14 ][ 15 ] A number of studies have specifically explored the influence of minority race on the experience of financial hardship after a cancer diagnosis.[ 16 ][ 17 ][ 18 ]

In a study using data from 3,242 lung and colorectal cancer survivors participating in the Cancer Care Outcomes Research and Surveillance Consortium (CanCORS) study, African American race was associated with an increased risk of self-reported economic burden relative to white race among patients with colorectal cancer (OR, 1.69; 95% CI, 1.24–2.30) after researchers adjusted for other sociodemographic and clinical factors.[ 17 ] This association was not seen among Hispanics with either lung or colorectal cancer or African Americans with lung cancer.

In another population-based survey of 3,133 women with breast cancer, Spanish-speaking women were at greater risk of financial decline related to breast cancer compared with whites (OR, 2.76; P = .006), whereas English-speaking Latinas and African-Americans did not share this increased risk.[ 16 ] In this same study, African-Americans and English-speaking Latinas were also more likely to report at least one privation as a result of breast cancer (i.e., economically motivated nonadherence or broader hardships related to medical expenses) compared with whites (OR, 2.62; P < .001 and OR, 2.17; P < .017, respectively), but this association was not seen with Spanish-speaking women.

Both analyses were adjusted for key demographic variables, including income, age, marital status, and education, which might also influence risk of financial hardship. Strong associations between minority race and financial hardship have not been demonstrated in other studies. However, these findings suggest that further research exploring the association between race and financial outcomes in cancer survivors is warranted.

Employment

Loss of productivity and employment can be considered both a risk factor for (predictor of) financial toxicity and a measure of financial toxicity (outcome). Several studies have shown that cancer patients experience loss of work, difficulty in returning to work, declines in income, and general loss of productivity as a result of cancer diagnoses.[ 1 ][ 18 ][ 19 ][ 20 ] Although employment and productivity loss can themselves be considered poor financial outcomes, employment loss has also been shown to be a risk factor for other material hardships, including debt and bankruptcy, whereas retirement has been shown to be protective.[ 8 ][ 10 ]

In an analysis of data from 1,202 adult cancer survivors from the 2011 MEPS Experiences with Cancer questionnaire, change in employment after diagnosis (switching to part-time work and taking extended leave) was associated with a substantially increased risk of material financial hardship compared with no change (49.1% vs. 20.2%; P < .001).[ 10 ] Particularly for the younger working-age population, loss of employment may be a mediator in the pathway between cancer diagnosis and financial toxicity.

Health Insurance

Patients who lack health insurance coverage are at elevated risk of many adverse experiences, including substantial financial hardship, particularly in an era of rapidly rising costs for cancer care. However, the presence of health insurance does not completely shield enrollees from high levels of out-of-pocket spending on health care services.

In the Medicare population, access to supplemental insurance and Medicare Part D plans has helped shield patients from some of the out-of-pocket cost burden. In an analysis of data from MEPS 2002–2010, outpatient prescription costs for adults older than 65 years decreased by 43% after the introduction of Medicare Part D, while younger patients (not yet Medicare-eligible) did not experience a similar decline in out-of-pocket expenditures for prescription drugs over the same period.[ 21 ] Another study found that supplemental insurance decreased older Medicare beneficiaries' risk of high out-of-pocket expenditures on cancer care.[ 6 ] Whether these protections against high out-of-pocket spending may translate into other decreases in material financial hardship, financial distress, debt, and bankruptcy is not clearly known.

The influence of type of insurance plan on the risk of financial hardship among younger patients (i.e., younger than 65 years) has not been thoroughly explored. One study found that patients with public insurance (Medicaid or Medicare) have an increased risk of financial hardship compared with patients who have private insurance (OR, 1.95; P < .0001).[ 8 ] However, having public health insurance may also be associated with fewer savings and assets and, therefore, increased financial vulnerability, factors that were not controlled for in this analysis.

参考文献- Dowling EC, Chawla N, Forsythe LP, et al.: Lost productivity and burden of illness in cancer survivors with and without other chronic conditions. Cancer 119 (18): 3393-401, 2013.[PUBMED Abstract]

- Allaire BT, Ekwueme DU, Guy GP, et al.: Medical Care Costs of Breast Cancer in Privately Insured Women Aged 18-44 Years. Am J Prev Med 50 (2): 270-7, 2016.[PUBMED Abstract]

- Kent EE, Forsythe LP, Yabroff KR, et al.: Are survivors who report cancer-related financial problems more likely to forgo or delay medical care? Cancer 119 (20): 3710-7, 2013.[PUBMED Abstract]

- Regenbogen SE, Veenstra CM, Hawley ST, et al.: The personal financial burden of complications after colorectal cancer surgery. Cancer 120 (19): 3074-81, 2014.[PUBMED Abstract]

- Guy GP, Yabroff KR, Ekwueme DU, et al.: Economic Burden of Chronic Conditions Among Survivors of Cancer in the United States. J Clin Oncol 35 (18): 2053-2061, 2017.[PUBMED Abstract]

- Davidoff AJ, Erten M, Shaffer T, et al.: Out-of-pocket health care expenditure burden for Medicare beneficiaries with cancer. Cancer 119 (6): 1257-65, 2013.[PUBMED Abstract]

- Ramsey S, Blough D, Kirchhoff A, et al.: Washington State cancer patients found to be at greater risk for bankruptcy than people without a cancer diagnosis. Health Aff (Millwood) 32 (6): 1143-52, 2013.[PUBMED Abstract]

- Banegas MP, Guy GP, de Moor JS, et al.: For Working-Age Cancer Survivors, Medical Debt And Bankruptcy Create Financial Hardships. Health Aff (Millwood) 35 (1): 54-61, 2016.[PUBMED Abstract]

- Shankaran V, Jolly S, Blough D, et al.: Risk factors for financial hardship in patients receiving adjuvant chemotherapy for colon cancer: a population-based exploratory analysis. J Clin Oncol 30 (14): 1608-14, 2012.[PUBMED Abstract]

- Yabroff KR, Dowling EC, Guy GP, et al.: Financial Hardship Associated With Cancer in the United States: Findings From a Population-Based Sample of Adult Cancer Survivors. J Clin Oncol 34 (3): 259-67, 2016.[PUBMED Abstract]

- Nathan PC, Henderson TO, Kirchhoff AC, et al.: Financial Hardship and the Economic Effect of Childhood Cancer Survivorship. J Clin Oncol 36 (21): 2198-2205, 2018.[PUBMED Abstract]

- Nipp RD, Kirchhoff AC, Fair D, et al.: Financial Burden in Survivors of Childhood Cancer: A Report From the Childhood Cancer Survivor Study. J Clin Oncol 35 (30): 3474-3481, 2017.[PUBMED Abstract]

- Chino F, Peppercorn J, Taylor DH, et al.: Self-reported financial burden and satisfaction with care among patients with cancer. Oncologist 19 (4): 414-20, 2014.[PUBMED Abstract]

- Sharrocks K, Spicer J, Camidge DR, et al.: The impact of socioeconomic status on access to cancer clinical trials. Br J Cancer 111 (9): 1684-7, 2014.[PUBMED Abstract]

- DiMartino LD, Birken SA, Mayer DK: The Relationship Between Cancer Survivors' Socioeconomic Status and Reports of Follow-up Care Discussions with Providers. J Cancer Educ 32 (4): 749-755, 2017.[PUBMED Abstract]

- Jagsi R, Pottow JA, Griffith KA, et al.: Long-term financial burden of breast cancer: experiences of a diverse cohort of survivors identified through population-based registries. J Clin Oncol 32 (12): 1269-76, 2014.[PUBMED Abstract]

- Pisu M, Kenzik KM, Oster RA, et al.: Economic hardship of minority and non-minority cancer survivors 1 year after diagnosis: another long-term effect of cancer? Cancer 121 (8): 1257-64, 2015.[PUBMED Abstract]

- Jagsi R, Ward KC, Abrahamse PH, et al.: Unmet need for clinician engagement regarding financial toxicity after diagnosis of breast cancer. Cancer 124 (18): 3668-3676, 2018.[PUBMED Abstract]

- Whitney RL, Bell JF, Reed SC, et al.: Predictors of financial difficulties and work modifications among cancer survivors in the United States. J Cancer Surviv 10 (2): 241-50, 2016.[PUBMED Abstract]

- Palmer JD, Patel TT, Eldredge-Hindy H, et al.: Patients Undergoing Radiation Therapy Are at Risk of Financial Toxicity: A Patient-based Prospective Survey Study. Int J Radiat Oncol Biol Phys 101 (2): 299-305, 2018.[PUBMED Abstract]

- Kircher SM, Johansen ME, Nimeiri HS, et al.: Impact of Medicare Part D on out-of-pocket drug costs and medical use for patients with cancer. Cancer 120 (21): 3378-84, 2014.[PUBMED Abstract]

- Consequences of Financial Toxicity Among Cancer Patients

-

Several retrospective cohort and cross-sectional studies have investigated the associations between financial burden from cancer care and treatment adherence, quality of life, satisfaction with care, incurring debt, filing for bankruptcy, and health outcomes. Cohort and cross-sectional studies are prone to study biases inherent to such study designs; therefore, caution must be exercised when interpreting the reported findings. Thus far, no evidence from randomized controlled clinical trials is available to guide patients and physicians about outcomes related to the financial toxicity among individuals diagnosed with cancer.

Access and Adherence to Treatments

Several retrospective cohort studies have evaluated the effect of prescription copayment amounts for cancer drugs on patient compliance with therapy.[ 1 ][ 2 ]

A cross-sectional study using data from the 2011 to 2014 National Health Interview Survey found that nonelderly individuals with a recent or previous cancer diagnosis were more likely to report changing their prescription drug use (e.g., not filling prescriptions or skipping doses) for financial reasons than those individuals without a history of cancer.[ 3 ] Another study examined the association between imatinib copayment and medication adherence among patients with chronic myeloid leukemia, from 2002 to 2011, using MarketScan health plan claims.[ 1 ] Over the study period, monthly copayments for imatinib ranged from $0 to $4,792, with a mean and median of $108 and $30, respectively. Patients in the highest quantile of monthly copayments for imatinib (mean, $53) compared with those patients in the lowest quantile (mean = $17) had a statistically significant adjusted risk ratio (RR) of 1.70 (95% confidence interval [CI], 1.30–2.22) for discontinuing imatinib during the first 180 days of treatment.[ 1 ] Similarly, patients with higher copayments for imatinib (vs. the lower copayment group) had an adjusted RR of 1.42 (95% CI, 1.19–1.69) for nonadherence to their imatinib therapy.[ 1 ]

Other studies examined the association between copayment amounts for adjuvant endocrine therapy, aromatase inhibitors (AIs), and tamoxifen and noncompliance in women with breast cancer.[ 2 ][ 4 ][ 5 ] Studies have been relatively consistent in showing that at the highest levels of copayment, cancer patients become less likely to take cancer-related medications on a daily basis (nonadherence), or they discontinue their medications over the long term (nonpersistence of use). Reduced adherence to cancer medications may be worse when the total out-of-pocket cost of all prescription drugs taken by the patient is considered.[ 5 ]

A cross-sectional survey study of adult patients (N = 300) receiving cancer therapy at Duke Cancer Institute found that 16% of patients reported high or overwhelming financial distress, 27% reported medication nonadherence, and 4.67% reported chemotherapy nonadherence.[ 6 ] Among patients reporting medication nonadherence, 14% specified skipping medication doses to make the prescription last longer, 11% stated they took less medication than prescribed to make the prescription last longer, and 22% indicated that they did not fill a prescription because of cost.[ 6 ] Among the patients reporting chemotherapy nonadherence, 1% skipped chemotherapy doses to make the prescription last longer, 1.67% took less chemotherapy to make the prescription last longer, and 3.33% did not fill a chemotherapy prescription because of cost.

Furthermore, this study found that an increased likelihood of nonadherence was associated with the following characteristics:

A statistically significant decreased risk of nonadherence was associated with having private insurance (adjusted OR, 0.31; 95% CI, 0.14–0.72).

A cross-sectional cohort study of 10,508 patients for whom oral chemotherapy was initiated between 2007 and 2009 examined the association between prescription abandonment rates and cost sharing.[ 7 ] Abandonment was defined as a paid prescription claim gap of more than 90 days. An adjusted analysis found that claims with cost sharing of $251 to $350 had 2.3 times the likelihood of abandonment (95% CI, 1.59–3.36); $351 to $500 had 3.28 times the likelihood of abandonment (95% CI, 2.20–4.88); and more than $500 had 4.46 times the likelihood of abandonment (95% CI, 3.80–5.22) when compared with cost sharing of $100 or less.[ 7 ] Additionally, the study identified a substantially higher proportion of patients who paid more than $500 out of pocket for their first oral chemotherapy claim in the Medicare group compared with the commercially insured group (45.5% vs. 10.7%; P < .001).[ 7 ]

Anecdotal reports also suggest that terminally ill cancer patients are foregoing the opportunity to obtain lethal doses of barbiturates in states with death-with-dignity laws because the price of these generic medications has increased to approximately $3,000 for a typical prescription.[ 8 ]

Quality of Life and Perceived Quality of Care

In a prospective, observational, population- and health care systems–based cohort study, the associations between financial burden, quality of life, and perceived quality of care were investigated using Cancer Care Outcomes Research and Surveillance Consortium (CanCORS) II data. Patient-reported health-related quality of life was measured using the EuroQol five-dimensions questionnaire (EQ-5D).

From 2003 to 2006, patients were enrolled in the U.S. CanCORS study within 3 months of receiving either a colorectal or lung cancer diagnosis. For the CanCORS II study, among the surviving CanCORS patients, one disease-free subcohort and one advanced-disease subcohort were selected and resurveyed about their quality of life. The median time from diagnosis was 7.3 years. An adjusted structural equation modeling analysis found that higher financial distress was negatively associated with health-related quality of life (adjusted beta, -0.06 per burden category; 95% CI, -0.08 to -0.05); however, financial distress was not associated with perceived quality of care (OR, 1.09; 95% CI, 0.93–1.29).[ 9 ] A lower perceived quality of care was associated with a poorer health-related quality of life (OR, 0.85; 95% CI, 0.79–0.92).[ 9 ] Moreover, having advanced disease was strongly associated with a poorer health-related quality of life (OR, -0.04; 95% CI, -0.08 to -0.01), but no association was observed with financial distress (OR,1.25; 95% CI, 0.79–1.98).[ 9 ]

Another cohort study using CanCORS data [ 10 ] found that financial strain was negatively associated with health-related quality of life and positively associated with symptom burden among patients with a lung or colorectal cancer diagnosis. Among lung cancer patients, those with fewer than 12 months of financial reserves to continue to live at their current standard of living reported increased symptom burden (adjusted mean difference, 5.25; 95% CI, 3.29–0.22), increased pain (adjusted mean difference, 5.03; 95% CI, 3.29–7.22), and lower quality of life (adjusted mean difference, 4.70; 95% CI, 2.82–6.58) compared with patients with more than 12 months of financial reserves.[ 10 ] Similarly, colorectal cancer patients with fewer than 12 months of financial reserves to continue to live at their current standard of living reported increased symptom burden (adjusted mean difference, 5.31; 95% CI, 3.58–7.04), increased pain (adjusted mean difference, 3.45; 95% CI, 1.25–5.66), and lower quality of life (adjusted mean difference, 5.22; 95% CI, 3.61–6.82) compared with those who reported more than 12 months of financial reserves.[ 10 ]

Several cross-sectional studies evaluated the impact of the financial burden of cancer care on patient quality of life. A survey analysis involving 149 advanced-stage cancer patients in the state of Texas at a public hospital (n = 72) and a comprehensive cancer center (n = 77) found that the median intensity of financial distress was double among patients treated in a public hospital compared with those treated in a comprehensive cancer center (on a scale of 0 = best to 10 = worst; 8 vs. 4; P = .0003).[ 11 ] More than 30% of patients perceived financial distress as being more severe than physical, emotional, social, or family distress.[ 11 ] Additionally, advanced-stage cancer patients in the public hospital reported the impact of financial distress relative to the impact of social and family distress as strongly agree, agree, or somewhat agree more frequently compared with patients treated in the comprehensive cancer center (54% vs. 33%, P = .0085).[ 11 ] Financial distress was inversely correlated with quality of life (r, -0.23; P = .0057).

A study of 2,108 patients from the 2010 National Health Interview Survey (NHIS) found that individuals who responded a lot (8.6%) to the survey question To what degree cancer causes financial problems for you and your family? were more likely to report the following when compared with those who reported no financial burden:[ 12 ]

Utilizing the 2011 Medical Expenditure Panel Survey (MEPS) data, one study [ 13 ] found that among 1,380 identified cancer survivors, 28.7% reported cancer-related financial burden. Additionally, cancer survivors who reported financial burden when compared with those who reported no financial burden were found to have the following outcomes:[ 13 ]

Satisfaction With Care

A review study documented that approximately 60% of people across a wide range of studies reported positive attitudes about cost-related discussions with their health care providers. Despite this, less than one-third of patients have had these discussions.[ 14 ] One study among women with breast cancer documented unmet need for engagement. Specifically, 72.8% of the 945 women who expressed worrying about finances at least somewhat indicated that cancer physicians and their staff did not help at least somewhat.[ 15 ] Additionally, 55.4% of the 523 women in the same study who expressed a desire to talk to health care providers about the impact of breast cancer on employment or finances reported that they had not had a relevant discussion with their cancer physicians, primary care providers, social workers, or other professionals.[ 15 ]

Financial Debt and Bankruptcy

Two studies considered the impact of the financial burden of cancer care on incurring debt and bankruptcy.[ 16 ][ 17 ]

One cross-sectional study, using the Livestrong 2012 survey data of 4,719 cancer survivors, reported that 63.8% of the survivors had worried about paying large bills related to cancer, 33.6% had gone into debt, 3.1% had filed for bankruptcy, and 39.7% had to make other kinds of financial sacrifices because of their cancer, its treatment, or the lasting effects of treatment.[ 16 ] Of those who reported going into debt, 9.1% had filed for bankruptcy, 55% incurred debt that totaled $10,000 or more, and 68% had to make other kinds of financial sacrifices because of the costs associated with their cancer care.[ 16 ]

Furthermore, this study found that an increased likelihood of filing for bankruptcy was associated with the following characteristics of cancer patients:[ 16 ]

Similar patient characteristics were reported for those going into medical debt.[ 16 ]

Another retrospective cohort study, using data from the 1995–2009 western Washington Surveillance, Epidemiology, and End Results (SEER) Cancer Registry–linked U.S. Bankruptcy Court for the Western District of Washington data, found that patients with cancer diagnoses were more likely (hazard ratio [HR], 2.65; P < .05) to file for bankruptcy compared with patients without cancer.[ 17 ] Thyroid cancer patients had the highest HR (HR, 3.46; P < .05).[ 17 ]

A clearly worded grading system has been developed to identify different levels of financial toxicity.[ 18 ] The usefulness of this system for categorizing and monitoring financial outcomes after cancer treatment has not been evaluated.

Impact on Caregivers

Informal cancer caregivers often share in the experience of financial toxicity by spending money on food, medications, and other patient needs in addition to taking time off from work to provide logistical, emotional, and medical support. In a recent survey of over 5,000 cancer patients whose caregivers were friends or family members, approximately 25% reported that their caregivers made significant employment changes after the cancer diagnosis, and 8% of survivors had caregivers who took at least 2 months of leave from work.[ 19 ] Evidence suggests that the cumulative financial and employment impacts of cancer caregiving can lead to higher caregiver burden, poorer quality of life, and poorer mental health among cancer caregivers.[ 20 ][ 21 ][ 22 ][ 23 ][ 24 ][ 25 ][ 26 ]

Terminally ill cancer patients from households reporting financial hardship had a higher likelihood of receiving intensive life-prolonging care (defined as receiving ventilation or resuscitation to prolong life) than did those who did not report financial hardship (OR, 3.22; 95% CI, 1.38−7.53). In a longitudinal survey of 281 terminally ill cancer patients, 29% reported using most or all of their household’s financial savings because of illness.[ 27 ]

Survival

In one retrospective cohort study of cancer patients who filed for bankruptcy compared with those who did not according to data in the western Washington SEER Cancer Registry, filing for bankruptcy was associated with an increased risk of mortality (adjusted HR, 1.79; 95% CI, 1.64–1.96).[ 28 ] Prostate cancer (adjusted HR, 2.07; 95% CI, 1.56–2.74) and colorectal cancer (adjusted HR, 2.47; 95% CI, 1.85–3.31) patients had the highest hazard ratios.[ 28 ]

Internal and External Validity Concerns With Observational Studies

Data from randomized controlled trials offer the strongest evidence for establishing the efficacy of treatment on cancer outcomes. However, because cancer patients cannot ethically be subjected to financial toxicity through randomization, the current body of evidence is primarily from observational data, particularly from cross-sectional and cohort studies. Large nationally representative surveys can provide the best estimates of the prevalence of certain conditions.

However, observational studies are prone to biases that may limit the validity of their findings. Several sources of bias are likely to be particularly important in observational studies assessing the association of financial toxicity with future outcomes, hence creating a challenge in interpreting the results of such studies.

In cross-sectional survey studies, high nonresponse rates may lead to the possibility of nonresponse bias in reported estimates if the potential answers of nonrespondents vary from those who did respond. Another source of bias in survey research is reporting bias, which refers to the selective revealing of information by respondents that they believe is more socially desirable.

Another source of bias in observational studies is reverse causality, which may weaken any true association between financial toxicity and its potentially related outcomes. In one study,[ 28 ] investigators provided an example of how the issue of reverse causality should be addressed in this type of work. In this instance, the authors performed a sensitivity analysis limiting their sample to early-stage cancer patients who declared bankruptcy within 1 year of diagnosis. They fit their previously developed Cox models, regressing survival on bankruptcy filing status, using this new population sample.

参考文献- Dusetzina SB, Winn AN, Abel GA, et al.: Cost sharing and adherence to tyrosine kinase inhibitors for patients with chronic myeloid leukemia. J Clin Oncol 32 (4): 306-11, 2014.[PUBMED Abstract]

- Neugut AI, Subar M, Wilde ET, et al.: Association between prescription co-payment amount and compliance with adjuvant hormonal therapy in women with early-stage breast cancer. J Clin Oncol 29 (18): 2534-42, 2011.[PUBMED Abstract]

- Zheng Z, Han X, Guy GP, et al.: Do cancer survivors change their prescription drug use for financial reasons? Findings from a nationally representative sample in the United States. Cancer 123 (8): 1453-1463, 2017.[PUBMED Abstract]

- Farias AJ, Du XL: Association Between Out-Of-Pocket Costs, Race/Ethnicity, and Adjuvant Endocrine Therapy Adherence Among Medicare Patients With Breast Cancer. J Clin Oncol 35 (1): 86-95, 2017.[PUBMED Abstract]

- Kim J, Rajan SS, Du XL, et al.: Association between financial burden and adjuvant hormonal therapy adherence and persistent use for privately insured women aged 18-64 years in BCBS of Texas. Breast Cancer Res Treat 169 (3): 573-586, 2018.[PUBMED Abstract]

- Bestvina CM, Zullig LL, Rushing C, et al.: Patient-oncologist cost communication, financial distress, and medication adherence. J Oncol Pract 10 (3): 162-7, 2014.[PUBMED Abstract]

- Streeter SB, Schwartzberg L, Husain N, et al.: Patient and plan characteristics affecting abandonment of oral oncolytic prescriptions. J Oncol Pract 7 (3 Suppl): 46s-51s, 2011.[PUBMED Abstract]

- Shankaran V, LaFrance RJ, Ramsey SD: Drug Price Inflation and the Cost of Assisted Death for Terminally Ill Patients-Death With Indignity. JAMA Oncol 3 (1): 15-16, 2017.[PUBMED Abstract]

- Zafar SY, McNeil RB, Thomas CM, et al.: Population-based assessment of cancer survivors' financial burden and quality of life: a prospective cohort study. J Oncol Pract 11 (2): 145-50, 2015.[PUBMED Abstract]

- Lathan CS, Cronin A, Tucker-Seeley R, et al.: Association of Financial Strain With Symptom Burden and Quality of Life for Patients With Lung or Colorectal Cancer. J Clin Oncol 34 (15): 1732-40, 2016.[PUBMED Abstract]

- Delgado-Guay M, Ferrer J, Rieber AG, et al.: Financial Distress and Its Associations With Physical and Emotional Symptoms and Quality of Life Among Advanced Cancer Patients. Oncologist 20 (9): 1092-8, 2015.[PUBMED Abstract]

- Fenn KM, Evans SB, McCorkle R, et al.: Impact of financial burden of cancer on survivors' quality of life. J Oncol Pract 10 (5): 332-8, 2014.[PUBMED Abstract]

- Kale HP, Carroll NV: Self-reported financial burden of cancer care and its effect on physical and mental health-related quality of life among US cancer survivors. Cancer 122 (8): 283-9, 2016.[PUBMED Abstract]

- Shih YT, Chien CR: A review of cost communication in oncology: Patient attitude, provider acceptance, and outcome assessment. Cancer 123 (6): 928-939, 2017.[PUBMED Abstract]

- Jagsi R, Ward KC, Abrahamse PH, et al.: Unmet need for clinician engagement regarding financial toxicity after diagnosis of breast cancer. Cancer 124 (18): 3668-3676, 2018.[PUBMED Abstract]

- Banegas MP, Guy GP, de Moor JS, et al.: For Working-Age Cancer Survivors, Medical Debt And Bankruptcy Create Financial Hardships. Health Aff (Millwood) 35 (1): 54-61, 2016.[PUBMED Abstract]

- Ramsey S, Blough D, Kirchhoff A, et al.: Washington State cancer patients found to be at greater risk for bankruptcy than people without a cancer diagnosis. Health Aff (Millwood) 32 (6): 1143-52, 2013.[PUBMED Abstract]

- Khera N: Reporting and grading financial toxicity. J Clin Oncol 32 (29): 3337-8, 2014.[PUBMED Abstract]

- de Moor JS, Dowling EC, Ekwueme DU, et al.: Employment implications of informal cancer caregiving. J Cancer Surviv 11 (1): 48-57, 2017.[PUBMED Abstract]

- Kent EE, Dionne-Odom JN: Population-Based Profile of Mental Health and Support Service Need Among Family Caregivers of Adults With Cancer. J Oncol Pract 15 (2): e122-e131, 2019.[PUBMED Abstract]

- Shin JY, Lim JW, Shin DW, et al.: Underestimated caregiver burden by cancer patients and its association with quality of life, depression and anxiety among caregivers. Eur J Cancer Care (Engl) 27 (2): e12814, 2018.[PUBMED Abstract]

- Ullrich A, Ascherfeld L, Marx G, et al.: Quality of life, psychological burden, needs, and satisfaction during specialized inpatient palliative care in family caregivers of advanced cancer patients. BMC Palliat Care 16 (1): 31, 2017.[PUBMED Abstract]

- Shaffer KM, Kim Y, Carver CS, et al.: Effects of caregiving status and changes in depressive symptoms on development of physical morbidity among long-term cancer caregivers. Health Psychol 36 (8): 770-778, 2017.[PUBMED Abstract]

- Rumpold T, Schur S, Amering M, et al.: Informal caregivers of advanced-stage cancer patients: Every second is at risk for psychiatric morbidity. Support Care Cancer 24 (5): 1975-1982, 2016.[PUBMED Abstract]

- Litzelman K, Kent EE, Rowland JH: Social factors in informal cancer caregivers: The interrelationships among social stressors, relationship quality, and family functioning in the CanCORS data set. Cancer 122 (2): 278-86, 2016.[PUBMED Abstract]

- Kent EE, Rowland JH, Northouse L, et al.: Caring for caregivers and patients: Research and clinical priorities for informal cancer caregiving. Cancer 122 (13): 1987-95, 2016.[PUBMED Abstract]

- Tucker-Seeley RD, Abel GA, Uno H, et al.: Financial hardship and the intensity of medical care received near death. Psychooncology 24 (5): 572-8, 2015.[PUBMED Abstract]

- Ramsey SD, Bansal A, Fedorenko CR, et al.: Financial Insolvency as a Risk Factor for Early Mortality Among Patients With Cancer. J Clin Oncol 34 (9): 980-6, 2016.[PUBMED Abstract]

- Evidence Gaps and Areas for Future Research

-

Considering the conceptual framework for cancer and its impact on health care use, health outcomes, and financial effects, based on extant models, allows exploration of current evidence, gaps in evidence, and areas for future research.[ 1 ][ 2 ]

Risk Factors

Although many individual risk factors for financial hardship have been identified, the evidence that demonstrates the degree to which these factors contribute to the risk of later financial hardship is insufficient, as is information about the interplay between these factors and clinical factors at the time of diagnosis.

Specific areas in need of further study to address their influence on the risk of financial distress after a cancer diagnosis include:

Because ample evidence exists that financial distress occurs even among patients with health insurance, the role that forms of insurance play in protecting individuals from financial distress requires further study. Medicare may at least partially protect older persons from financial harm; however, in addition to this universal benefit for persons older than 65 years, other factors that are associated with older age might also reduce the risk of financial distress, namely, retired adults typically have higher levels of assets (e.g., owning a home outright), pensions or retirement accounts as sources of income, and Social Security. Another factor is that physicians may treat older patients less intensively and thus less expensively.

For adults of working age, characteristics of work-sponsored or individually purchased commercial insurance that vary from plan to plan—specifically, deductibles, copay levels, and coverage exclusions—may influence the risk of financial distress. These factors also warrant further study.

After patients are diagnosed with cancer and miss work during treatment, their ability to continue to work or return to work greatly influences their future risk of financial hardship. Studies are needed that relate particular treatments, modalities of treatment (e.g., infusional therapy vs. oral therapy), and toxicities of treatments with work absenteeism, loss of productivity, and likelihood of returning to the workforce.

Implementation of the U.S. Affordable Care Act in 2008 provided a natural experiment to determine whether expanding access to health insurance for millions of Americans had an impact on rates of financial distress or insolvency for persons with cancer. Proposed pilots for different Medicare payment systems may also offer opportunities for quasi-experimental approaches that compare implementation with nonimplementation.[ 3 ]

After diagnosis, treatment choice could, in theory, influence the likelihood of experiencing financial difficulties. For many cancers, guidelines include options that are considered equivalent therapeutically, yet the costs of the treatments might vary by 50-fold or more.[ 4 ] Oral medications, for example, may come under a different copay structure than office-administered medicines. No retrospective or prospective evidence exists to show that, within an indication such as tumor type and stage, choice of treatment has a differential impact on out-of-pocket expenditure or level of financial distress. Because treatment choice is influenced by many factors, including, at least potentially, the financial situation of the patient, prospective studies with detailed clinical and financial information are needed to investigate this issue.

Cancer management is unusual among medical interventions because intensive treatment at specialized facilities for weeks or months is often involved. For many patients, nonmedical costs associated with seeking treatment, such as the cost of transportation and lodging during treatment, can take a financial toll on families. The role that nonmedical costs play in financial hardship is an area in need of further study.

Financial Distress and Outcomes

Evidence from multiple retrospective studies shows that patients experiencing financial distress have reduced adherence to planned therapies, lower quality of life, and diminished survival. These studies have limitations because certain unmeasured clinical and financial factors that may influence treatment choice might also influence outcomes. Prospective or retrospective studies that include a more-comprehensive picture of financial status at diagnosis and clinical and patient factors that might influence treatment choice would provide a more accurate picture of the causal pathway between financial distress and outcomes.

Interventions Aimed at Reducing Financial Distress Among Cancer Patients

Several interventions specifically designed to reduce rates of financial distress among cancer patients have been proposed. Some are being implemented, but, to date, there have been no prospective studies evaluating the impact of these interventions on the rates and severity of financial distress, care choices, quality of life, or survival. Several of the most commonly discussed interventions are reviewed below.

Financial navigators

Financial navigators are being used in community and academic settings to help cancer patients avoid adverse financial consequences after a cancer diagnosis.[ 5 ] The impact of these programs on patients’ financial and health outcomes is an area for future study. Specific issues of interest include:

One prospective study (S1417CD [NCT02728804]) being conducted in the National Cancer Institute Cooperative Cancer Clinical Trials Network, Implementation of a Prospective Financial Impact Assessment Tool in Patients with Metastatic Colorectal Cancer, is evaluating the incidence of treatment-related financial hardship among patients with newly diagnosed metastatic colorectal cancer.[ 6 ] In addition to detailed clinical information, patient credit history at baseline and throughout treatment, health-related quality of life, out-of-pocket costs, treatment nonadherence, and caregiver burden is being measured over 12 months.

Price transparency to facilitate treatment choice

Studies of price transparency initiatives, such as one that required California hospitals to publish their charges, have not found that they significantly influence patient treatment choice or pricing of goods and services by health care providers.[ 7 ] Looking at price transparency and provider behavior, one controlled study found that providing clinicians with information about test costs in electronic medical record order-entry forms reduced the number of tests ordered compared with not providing this information.[ 8 ] It is not known whether providing price transparency would alter cancer patient or clinician choices for care.

More information is needed regarding how responsive cancer patients, their families, and/or their providers might be to offers of pricing transparency, direct or indirect financial assistance, or further reductions in out-of-pocket payment requirements.

Value-based pricing

Closely related to price transparency is the concept of value-based pricing: a concept in which patients’ out-of-pocket expenditures are tied to external assessment of value for competing therapies for particular conditions. The objective of value-based pricing is to steer patients to higher-value therapies through financial incentives (higher value = lower out-of-pocket responsibility). Although value-based pricing has been implemented for several clinical conditions (e.g., hypertension, diabetes), and evidence exists that this type of pricing increases the utilization of higher-value services, it has not been applied in oncology. Because of the ongoing transformation in how medical providers are paid for the care of cancer patients, we need to better identify opportunities and challenges to increasing awareness of and solutions to patient financial toxicity in the context of alternative payment models and quality measure reforms.

It is also unclear when in the care trajectory more information and financial assistance are needed and will be most effective in encouraging treatment initiation and continuance. For example, most employer-based insurance policies have an annual out-of-pocket maximum, beyond which the insurer assumes 100% of the cost of care. Many patients with late-stage cancer reach the maximum quickly, in which case the insurer bears the full cost of anticancer treatments for the remainder of the benefit year.

Health insurance reform

By providing millions of previously uninsured Americans with health insurance, the Massachusetts health insurance plan and the U.S. Affordable Care Act have presented an opportunity for natural pre-post experiments for health care policies that are aimed at reducing the financial exposure of an individual during severe illness. Because insurance appears to mitigate rather than eliminate the risk of financial distress from a cancer diagnosis and treatment, other interventions aimed at improving financial outcomes for insured persons are likely needed.

Another policy targeting providers and patients would be to require the use of patient decision aids that include benefits-cost and financial-toxicity assessments and assistance through measures-of-quality for fee-for-service Medicare payments under Medicare Access and CHIP (Children’s Health Insurance Program) Reauthorization Act (MACRA) legislation.[ 9 ][ 10 ] Pursuit of this policy would require endorsement by the Centers for Medicare and Medicaid Services and possibly legislation enacted by the U.S. Congress.

Reducing and/or eliminating patient copayment/coinsurance for pathway-adherent cancer care in the fee-for-service Medicare program and/or commercial plans would also likely act to reduce patient and family burden across multiple treatment modalities—radiation, drugs, inpatient and outpatient coinsurance, and copayments.[ 7 ][ 8 ] Another set of policies would eliminate the ban on pharmaceutical manufacturer-provided couponing and other patient-assistance programs to Medicare beneficiaries.[ 11 ]

Cancer Treatment Costs References

Cancer treatment cost information can be difficult to access. Listed below are links to publicly available websites that contain updated information on costs related to cancer care:

参考文献- Smith R, Clarke L, Berry K, et al.: A comparison of methods for linking health insurance claims with clinical records from a large cancer registry. [Abstract] Med Decis Making 21 (6): 530, 2001.[PUBMED Abstract]

- Fay S, Hurst E, White MJ: The household bankruptcy decision. Am Econ Rev 92 (3): 706-18, 2002.[PUBMED Abstract]

- Centers for Medicare & Medicaid Services: Oncology Care Model. Baltimore, Md: Centers for Medicare & Medicaid Services, 2016. Available online. Accessed December 8, 2016.[PUBMED Abstract]

- Ramsey S, Shankaran V: Managing the financial impact of cancer treatment: the role of clinical practice guidelines. J Natl Compr Canc Netw 10 (8): 1037-42, 2012.[PUBMED Abstract]

- Conti RM, Bach PB: The 340B drug discount program: hospitals generate profits by expanding to reach more affluent communities. Health Aff (Millwood) 33 (10): 1786-92, 2014.[PUBMED Abstract]

- Shankaran V; Southwest Oncology Group Cancer Care Delivery, Gastrointestinal Cancer: Implementation of a Prospective Financial Impact Assessment Tool in Patients with Metastatic Colorectal Cancer. April 15, 2016.[PUBMED Abstract]

- Kline RM, Bazell C, Smith E, et al.: Centers for medicare and medicaid services: using an episode-based payment model to improve oncology care. J Oncol Pract 11 (2): 114-6, 2015.[PUBMED Abstract]

- Newcomer LN, Gould B, Page RD, et al.: Changing physician incentives for affordable, quality cancer care: results of an episode payment model. J Oncol Pract 10 (5): 322-6, 2014.[PUBMED Abstract]

- Cutler DM: Payment reform is about to become a reality. JAMA 313 (16): 1606-7, 2015.[PUBMED Abstract]

- Press MJ, Rajkumar R, Conway PH: Medicare's New Bundled Payments: Design, Strategy, and Evolution. JAMA 315 (2): 131-2, 2016.[PUBMED Abstract]

- Howard DH: Drug companies' patient-assistance programs--helping patients or profits? N Engl J Med 371 (2): 97-9, 2014.[PUBMED Abstract]

- Changes to This Summary (09/18/2019)

-

The PDQ cancer information summaries 2019-08-022019-08-02are reviewed regularly and updated as new information becomes available. This section describes the latest changes made to this summary as of the date above.

Consequences of Financial Toxicity Among Cancer Patients

Revised text to state that in a recent survey of over 5,000 cancer patients whose caregivers were friends or family members, approximately 25% reported that their caregivers made significant employment changes after the cancer diagnosis, and 8% of survivors had caregivers who took at least 2 months of leave from work.

This summary is written and maintained by the PDQ Adult Treatment Editorial Board, which is editorially independent of NCI. The summary reflects an independent review of the literature and does not represent a policy statement of NCI or NIH. More information about summary policies and the role of the PDQ Editorial Boards in maintaining the PDQ summaries can be found on the About This PDQ Summary and PDQ® - NCI's Comprehensive Cancer Database pages.

- About This PDQ Summary

-

Purpose of This Summary

This PDQ cancer information summary for health professionals provides comprehensive, peer-reviewed, evidence-based information about the treatment of cancer and financial toxicity. It is intended as a resource to inform and assist clinicians who care for cancer patients. It does not provide formal guidelines or recommendations for making health care decisions.

Reviewers and Updates

This summary is reviewed regularly and updated as necessary by the PDQ Adult Treatment Editorial Board, which is editorially independent of the National Cancer Institute (NCI). The summary reflects an independent review of the literature and does not represent a policy statement of NCI or the National Institutes of Health (NIH).

Board members review recently published articles each month to determine whether an article should:

Changes to the summaries are made through a consensus process in which Board members evaluate the strength of the evidence in the published articles and determine how the article should be included in the summary.

Any comments or questions about the summary content should be submitted to Cancer.gov through the NCI website's Email Us. Do not contact the individual Board Members with questions or comments about the summaries. Board members will not respond to individual inquiries.

Levels of Evidence

Some of the reference citations in this summary are accompanied by a level-of-evidence designation. These designations are intended to help readers assess the strength of the evidence supporting the use of specific interventions or approaches. The PDQ Adult Treatment Editorial Board uses a formal evidence ranking system in developing its level-of-evidence designations.

Permission to Use This Summary

PDQ is a registered trademark. Although the content of PDQ documents can be used freely as text, it cannot be identified as an NCI PDQ cancer information summary unless it is presented in its entirety and is regularly updated. However, an author would be permitted to write a sentence such as “NCI’s PDQ cancer information summary about breast cancer prevention states the risks succinctly: [include excerpt from the summary].”

The preferred citation for this PDQ summary is:

PDQ® Adult Treatment Editorial Board. PDQ Financial Toxicity and Cancer Treatment. Bethesda, MD: National Cancer Institute. Updated <MM/DD/YYYY>. Available at: https://www.cancer.gov/about-cancer/managing-care/track-care-costs/financial-toxicity-hp-pdq. Accessed <MM/DD/YYYY>. [PMID: 27583328 ]

Images in this summary are used with permission of the author(s), artist, and/or publisher for use within the PDQ summaries only. Permission to use images outside the context of PDQ information must be obtained from the owner(s) and cannot be granted by the National Cancer Institute. Information about using the illustrations in this summary, along with many other cancer-related images, is available in Visuals Online, a collection of over 2,000 scientific images.

Disclaimer

Based on the strength of the available evidence, treatment options may be described as either “standard” or “under clinical evaluation.” These classifications should not be used as a basis for insurance reimbursement determinations. More information on insurance coverage is available on Cancer.gov on the Managing Cancer Care page.

Contact Us

More information about contacting us or receiving help with the Cancer.gov website can be found on our Contact Us for Help page. Questions can also be submitted to Cancer.gov through the website’s Email Us.